Never heard of Quantpedia?

Quantpedia titles itself as "the encyclopedia of quantitative trading strategies." Whereas quantitative analysis focuses on mathematical and statistical modeling, I've found Quantpedia is an abundant source of fundamental and value trading strategy ideas. All their results are self-reported, and they usually only apply to time periods way in the past. Let's plug one of their strategies into Genovest, and see how well it holds up.

Net Current Asset Value Effect

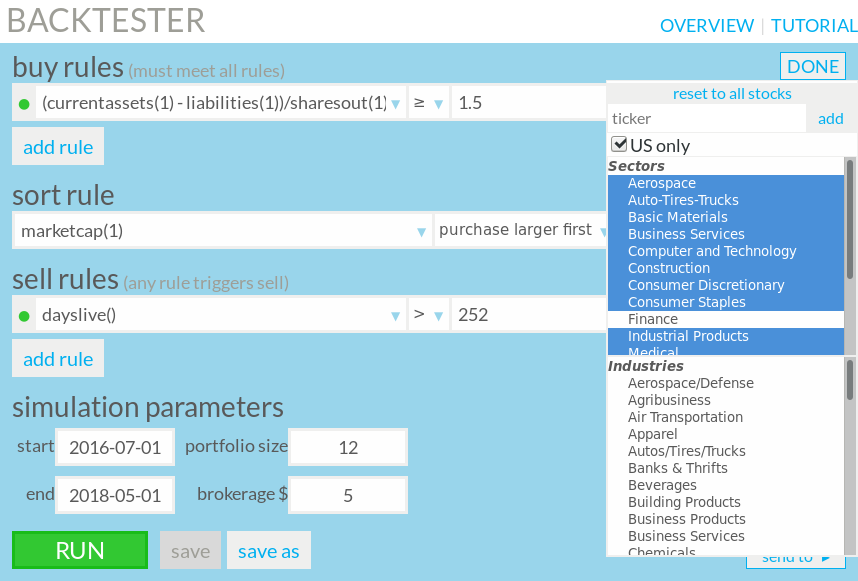

Of the strategies Quantpedia has available for free, Net Current Asset Value Effect seemed like the perfect one to test first. It's purely a fundamental strategy, and is inspired by one of our favorite famous investors, Benjamin Graham. The net current asset value (NCAV), as defined by Graham, is current assets minus all liabilities, divided by the number of shares outstanding market cap (See Jan 4, 2020 edit). Graham claimed that companies with a higher NCAV were often under-priced compared to the true underlying value of the company.

Jan 4, 2020 edit: We had an anonymous reader write in to us, pointing out that we should be dividing my market cap, not the number of shares outstanding. Thank you, whoever you are! I misread the original Quantpedia article. Technically NCAV is just current assets minus liabilities. Dividing by market cap will give you a scaled NCAV that you can use to compare across companies, regardless of size. What's interesting however is, my "flawed" strategy produced decent returns. When I tested with the modified formula

(currentassets(1)-liabilities(1))/marketcap(1)returns were much more volatile, and less desirable in my opinion. This highlights a key strength of Genovest - you are empowered to think outside the realm of conventional wisdom, and discover new ways of thinking that give you a competitive edge in the market. It might not make sense at first to divide by shares, but it points to areas for exploration, and it's hard to argue with consistent returns!

Getting specific, the strategy instructs the investor to only buy stocks with NCAV over 1.5, exclude lightly-regulated companies, and exclude companies in the financial sector. The portfolio of stocks is formed annually in July, and held for one year with equal weighting. The strategy comes from an academic paper out of London, which also excluded foreign companies. Since Genovest services mainly US based investors, we'll run the analysis on US companies, which will also remove lightly-regulated companies.

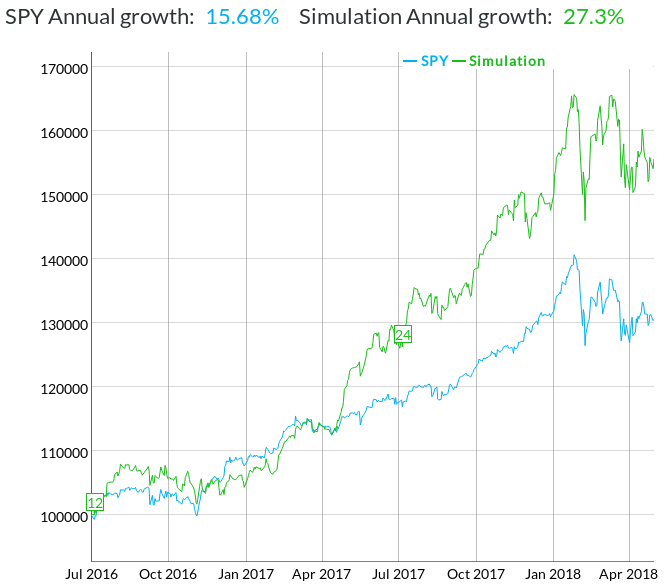

The original paper this strategy came from was published in 2007, and claimed to make 19.7% annualized return when tested from 1981 to 2005. That was over ten years ago - let's put it to the test in today's market!

Deceptively simple rules

Plugging the rules into the Genovest Backtester was pretty easy, since we support mathematical formulas. The strategy suggests to hold 100 stocks, but in my humble opinion, that is far too many for the individual investor to keep track of. Furthermore, it doesn't indicate how you should sort the stocks to arrive at your top picks, so we'll use the Genovest default of the top 12 companies by market capitalization.

It's not often I'm surprised by a trading strategy, but this had me floored. Normally it takes some fine-tuning of the rules, and experimenting with different financial metrics before I get a result this consistent and strong. Obviously I'll need to test this over different time periods, see if it's sensitive to only starting in July, try some stop-loss or profit taking rules just to be safe, and remove penny stocks, but this is a great start. The insight of Benjamin Graham holds true, even in modern times!

Conclusion

Quantpedia has hundreds of strategies, some of which are free, like the one we looked at in this post. They aim to aggregate academic research, and plainly lay out the practical nuts and bolts of the research. Finding which ones work in contemporary markets is the real challenge, since the papers only capture results from when they were published, and are often retrospective even at that time. Having a backtester solves these key problems, and allows you to act on research with confidence.